Is Arabica Washed Out? - 25 Magazine: Issue 2

While demand for washed arabica beans is soaring, total output has remained stagnant for two decades and is now rapidly losing market share at origin.

THOMAS COPPLE asks if specialty coffee is in danger of becoming a victim of its own success.

Washed arabicas – the lifeblood of the specialty sector – are under pressure. While there are some great naturally processed coffees, and even some specialty robustas, washed arabicas are the industry’s most prized coffees. The trouble is they’re only grown in a handful of countries, and the total output from these origins has barely changed for over 20 years. As specialty coffee consumption continues to thrive, and new markets open up, this supply will be squeezed tightly as competition intensifies.

The Dominance of Brazil and Vietnam

Worldwide coffee consumption is growing at nearly 2% per year, with some markets recording growth rates of over 10%. Every year global demand breaks new record highs, and now sits on around 156 million 60 kg bags, up from under 100 million in 1995. The specialty coffee industry is clearly one factor behind this resurgence, though demographic and economic growth in new and emerging markets are also hugely significant.

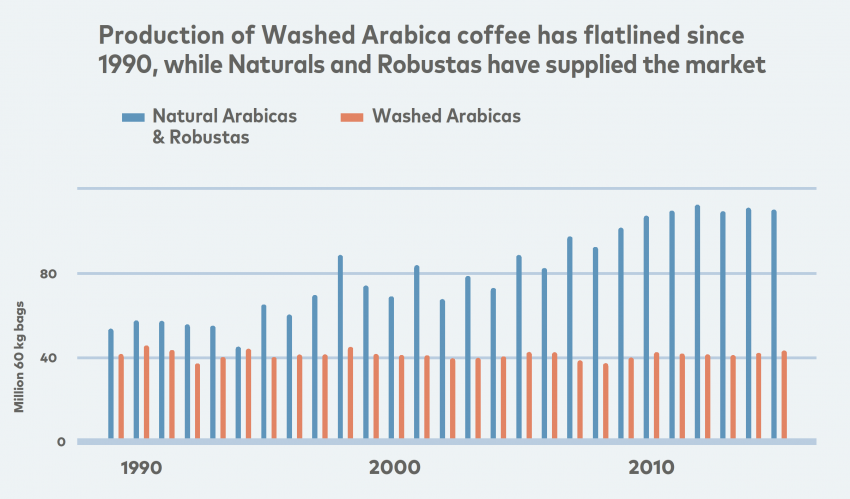

Although Brazil and Vietnam have more than doubled their annual production in the last 25 years, producers of washed Arabicas have stayed largely the same, at around 40 million bags per year. As a result, despite its increasing prevalence at the point of consumption, specialty coffee is rapidly losing market share at origin.

At the same time, global supply is increasing to fuel this demand. Since the year 2000, total production of coffee has jumped by over a third to reach 152 million bags in 2016. But this growth is not equally distributed. In fact, 90% of this additional supply has come from just two countries: Brazil and Vietnam, who between them now account for over 50% of all coffee production worldwide. The growth of Brazil and Vietnam means that most new supply is either in robustas or naturally processed arabicas. Other origins, particularly those producing washed Arabica coffees, have not been so successful.

What Does This Mean for Specialty?

Defining and measuring the spread of specialty coffee is difficult. Definitions vary from region to region, from person to person. Even the idea of quality is fluid, and subject to interpretation.

That said, washed arabica coffees, or what green coffee traders call ‘Milds’, are generally considered the best quality beans in the coffee trade, commanding the highest prices. They typically result in a cleaner, more consistent cup, which can be particularly useful when highlighting the flavor profile of single-origin coffees.

Growing these high-quality beans requires specific climatic conditions – rainfall, temperature, and sunlight – which can only be found in a few altitudinous locations worldwide. Most washed arabica coffees therefore come from just a few regions, predominantly from South and Central America and East Africa, with Colombia producing the largest volumes.

While we have limited data on the supply and demand of specialty coffee specifically, examining washed Arabicas is a pretty good proxy, and the trends are concerning. Although Brazil and Vietnam have more than doubled their annual production in the last 25 years, producers of washed arabicas have stayed largely the same, at around 40 million bags per year. As a result, despite its increasing prevalence at the point of consumption, specialty coffee is rapidly losing market share at origin.

Why Has This Happened?

The causes behind the stagnation in production of washed arabica coffees are many and varied. Not all countries have undergone the same path. In Colombia, for example, arabica production was devastated by an outbreak of coffee leaf rust in 2008, and is only now recovering to its previous volumes following a massive and costly replanting program.

Another outbreak of rust, this time in 2013, tore through much of Central America, resulting in the loss of hundreds of thousands of jobs and millions of bags of lost output. Many countries have still not recovered.

In addition to pests and disease, the coffee crisis in the early 2000s, when international prices dropped below 50 cents/lb., forced many producers out of the market permanently. Competition from other cash crops has become fierce, while increased land use pressure, particularly the demand for real estate from expanding urban areas, has rendered coffee inherently unappealing. Nairobi, Kenya is a prime example, where farmers are selling their coffee farms to developers for apartments, shopping malls, and other commercial purposes.

Subsequently, some of your favorite coffee origins have collapsed in volume since 1990. El Salvador is down from three million bags in 1992 to just 620,000 today, while Costa Rica, Kenya, and Mexico are all about 50% lower compared to their early 1990s peaks.

Even in countries that have seen increases, the outlook is far from perfect. Ethiopia has more than doubled its output over the last 25 years, but it is on the frontline of climate change, in danger of losing up to 60% of its growing area by the end of this century, according to a recent study published by the Royal Botanic Gardens, Kew. Peru and Honduras have also seen strong increases, but both are now facing their own battles with coffee leaf rust. The recent discovery that rust- resistant varieties in Honduras have been infected adds a new level of concern. And so, while the major washed arabica producing countries have seen mixed fortunes over the last 25 years, for many countries the end result has been disastrous.

Prospects for the Future

The problems facing the production of washed arabicas are not expected to go away any time soon. The triple threats of climate change, aging farmers, and unremunerative prices are already a reality for many producers, and the high-quality varieties that are so valued in the specialty coffee industry, like Bourbon, Geisha, or SL28, are also those most at risk.

Looking ahead to the future, if washed arabicas maintain their current production volumes of around 40 million bags per year, they could account for just 21% of world production by 2030. Even maintaining this level is not guaranteed. The fact that the overall total has remained so steady for so long is due in large part to the efforts of just a few countries, particularly those with strong domestic coffee institutions, such as the National Federation of Coffee Growers of Colombia (FNC) or the Coffee Institute of Honduras (IHCAFE).

As the effects of climate change become ever more apparent, it is going to be harder to sustain this level of output. The optimum area available for coffee production is going to change, and in many cases will require significant upheaval to move to new pastures. As coffee trees get older, they become less productive and more prone to disease, requiring replacing and replanting. Urbanization and economic development increase the price of land and also offer improved opportunities to younger generations, who might not want to be coffee farmers any more. The specialty coffee industry will be competing for an ever-decreasing share of the coffee pie.

What Can We Do?

The key to securing specialty coffee’s future is collaboration. We must strengthen linkages between producers and consumers in order to ensure that their incentives are aligned. Currently, the inherent volatility in international coffee prices, and the unpredictability of potential returns, acts as a deterrent for many producers. For specialty coffee to be truly sustainable, buyers need to identify farmers, and vice-versa, so that coffee is effectively grown to order.

There is an urgent and immediate need for investment in coffee research. Washed arabica coffees are generally the most susceptible to weather shocks, to changes in the climate, and to outbreaks of disease like rust. We need to better understand the effects of these changes and how best to adapt. Some of this work is already happening, but it needs to be ramped up and that requires finance.

Finally, we need as an industry to continue promoting the consumption of quality coffee. By establishing a clear and reliable market for specialty coffee, the industry can encourage sustainable production, and paying a premium for quality can ensure that there is an incentive for producers to remain in the market. The challenges facing specialty coffee production are real and immediate, but they are not yet insurmountable.

THOMAS COPPLE is a researcher and analyst and a former economist at the International Coffee Organization.